2025 Annual results

-4.5%

Organic decline

8.5% of revenue

Operating profit on activities

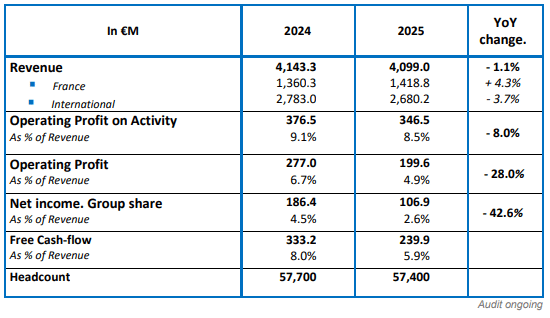

BUSINESS IN 2025: -1.1%

At end‑December, activity shows a decline of –1.1%: +4.3% in France and –3.7% outside France. On a like‑for‑like and constant‑exchange‑rate basis, activity declined by –4.5% (–3.6% in France and –4.9% outside France).

Activity in the fourth quarter was better than expected. Civil Aeronautics and Banking/Finance sectors returned to growth.

The decline in activity in 2025 is mainly due to a sharp drop in the Automotive sector (–16%) and, to a lesser extent, in Telecoms, Other Industries, Electronics, and the Public Sector. Defence/Security & Naval, as well as Energy, posted significant growth.

Southern Europe continues to grow satisfactorily; Eastern Europe and APAC are stable. Other regions remain in decline, though the situation is gradually improving, except in the UK, Benelux, and the Nordics.

OPERATING MARGIN ON ACTIVITY: 8.5% OF REVENUE

Beyond the unfavorable calendar effect, challenging economic conditions in several countries (Germany and the Nordics) weighed on the Group’s operating margin on activity.

Lower SG&A costs, good utilization rates, and efficient project management enabled the Group to deliver an operating profit from ordinary activities of €346.5m, representing 8.5% of revenue -above the anticipated level (8.1%).

OPERATING PROFIT: 4.9% OF REVENUE

Operating profit amounts to €199.6m. It includes €21.0m in share‑based payments, €12.2m in amortization of intangible assets (customer relationships/order backlog) from the purchase price allocation of Worldgrid, €67.4m in goodwill impairment, €46.3m in non‑recurring costs, comprising €21.5m related to the French Competition Authority fine (disputed on appeal), €3.7m in acquisition fees, €1.4m in earn‑out adjustments, €2m related to tax and social inspections, €17.6m in restructuring costs internationally.

NET PROFIT – GROUP SHARE: 2.6% OF REVENUE

The financial result amounted to -€4,0 m after taking into account the tax expense of €88.5 m, the Group’s net profit came to €106.9 m.

NET CASH POSITION: €390.2M / GEARING: – 17.5%

Cash flow (excluding IFRS16) amounted to €317.5 m (7.7% of revenue).

Working capital requirements decreased by €33.5 m, mainly due to an improvement in DSO and the organic decline in activity. Taxes paid totaled €97.1 m and Capex remained low (€11.8 m, i.e. 0.3% of revenue). As a result, free cash flow reached €239.9 m, representing 5.9% of revenue (-28% vs. 2024).

After taking into account net financial investments – mainly acquisitions (- €62.9 m), dividends paid

(- €52.2 m), and other financing flows (- €10.1 m), net cash amounted to +€390.2 m at end‑December 2025.

ALTEN self‑financed its external growth and dividends and retains significant investment capacity (gearing: –17.5%).

EXTERNAL GROWTH:

4 ACQUISITIONS in 2025

- In the US and India: Company specialized in Life science

(Revenue: €7.5M, 120 consultants)

- In India: Company specialized in embedded software, mainly for the automotive industry

(Revenue: €5.2 M, 270 consultants).

- In Spain & South America: Company specialized in Digital Transformation

(Revenue: €19M, 300 consultants)

- In France & Belgium: Company specialized in Life Sciences

(Revenue: €20.5M, 190 consultants)

OUTLOOK FOR 2026 :

Q4 2025 indicates a gradual sequential stabilization across most sectors, while Civil Aeronautics and Banking/Finance have returned to growth.

Visibility nevertheless remains limited at the start of the year. The first quarter of 2026 should confirm this trend reversal and help refine the outlook for the full year.

Next release: 28 April after market close— Q1 2026 Activity